Singapore Private Residential Market Overview Transactions, Prices, the Absorption Truth & Market Segments (2021–2026)

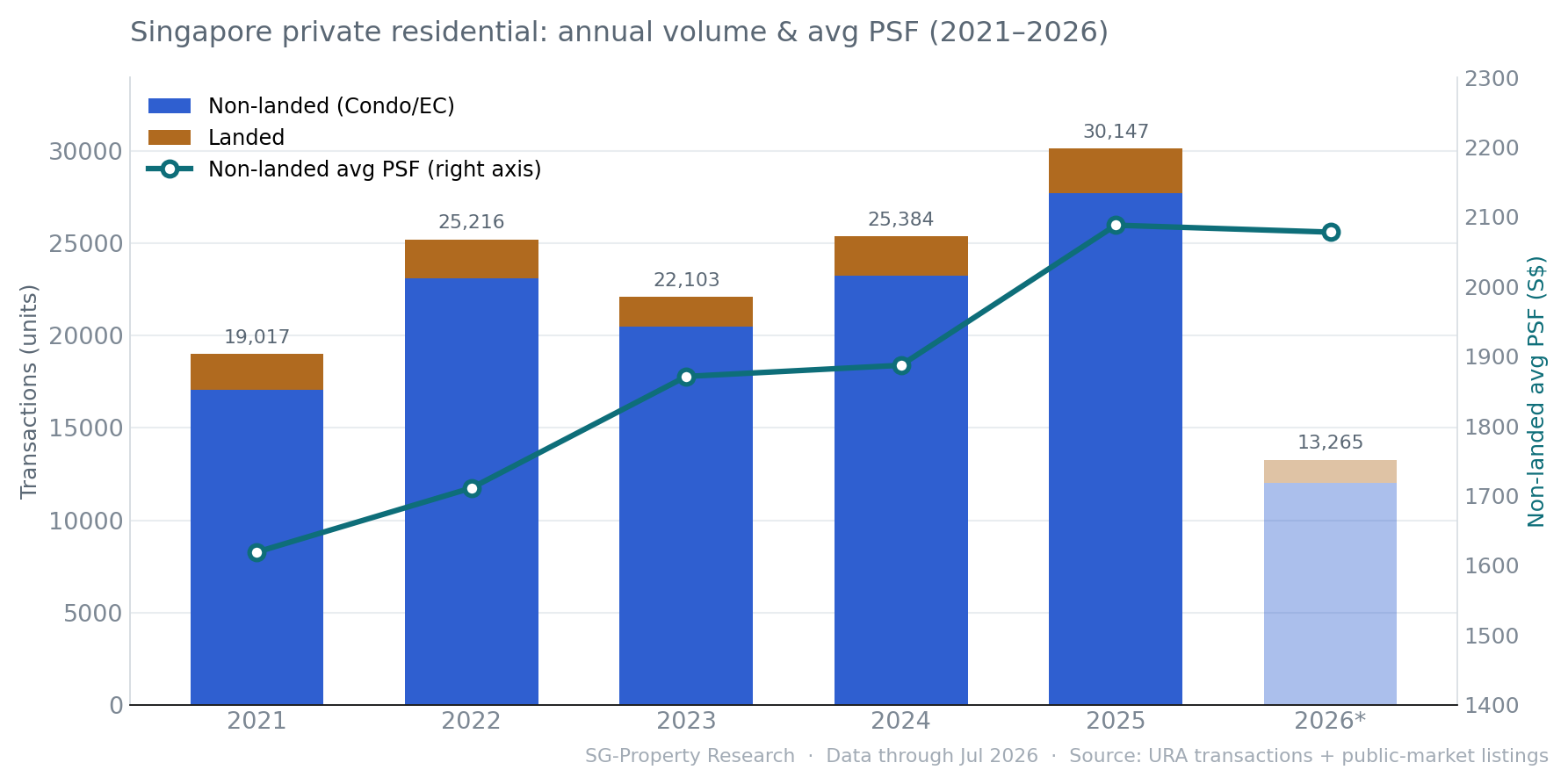

- Market size: Singapore private residential transactions reached about 30,000 units in 2025, a multi-year high; the non-landed (condo/EC) average PSF rose a cumulative +28.4% over five years ($1,619 → $2,078).

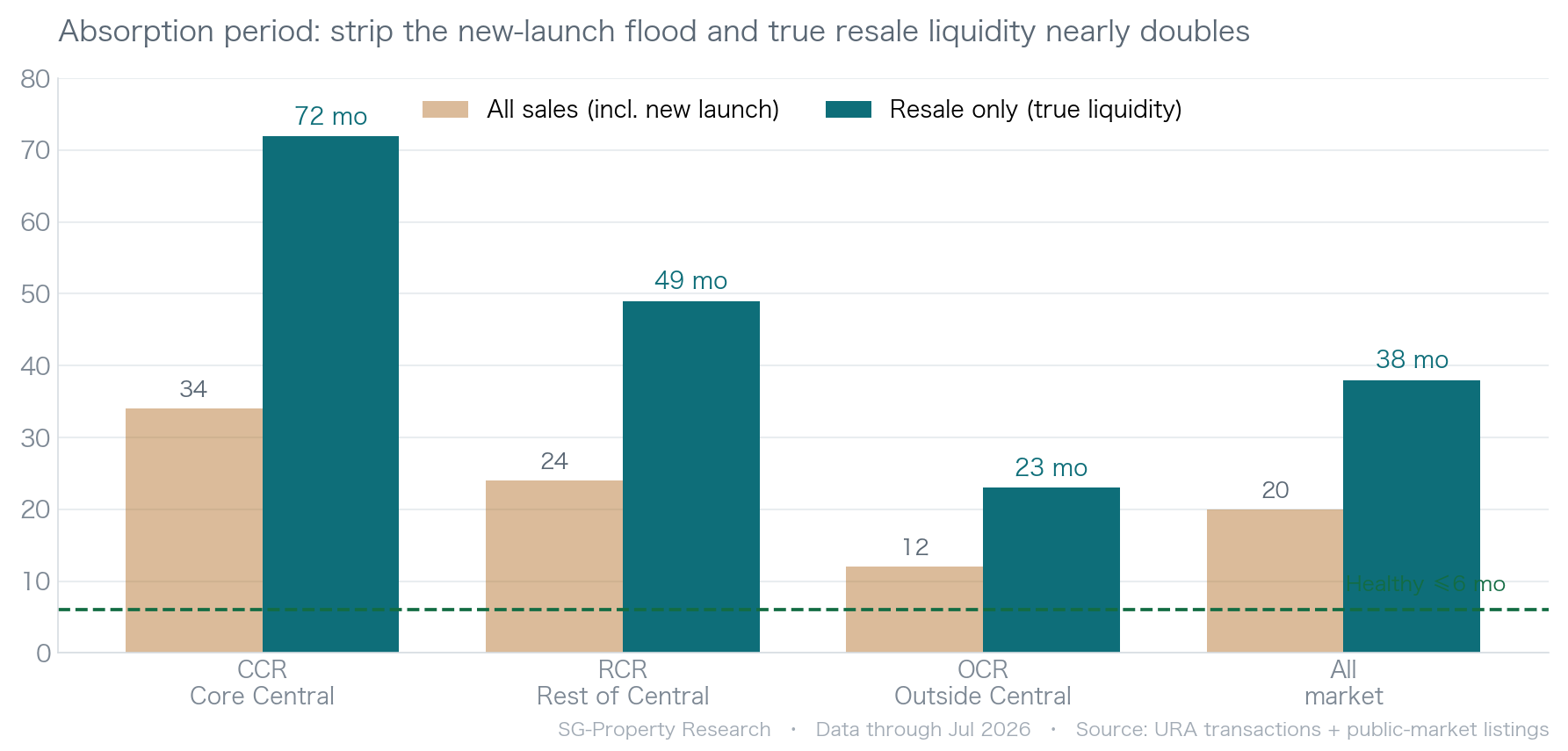

- The absorption truth (this report's core): counting new launches, market-wide absorption reads just 20 months; strip them out and count resale only, and it stretches to 38 months — nearly double, and this is the true resale liquidity.

- The new-launch flood: new-launch transactions surged to about 12,000 units in 2025; concentrated releases sped up overall transactions and masked the resale market's absorptive capacity.

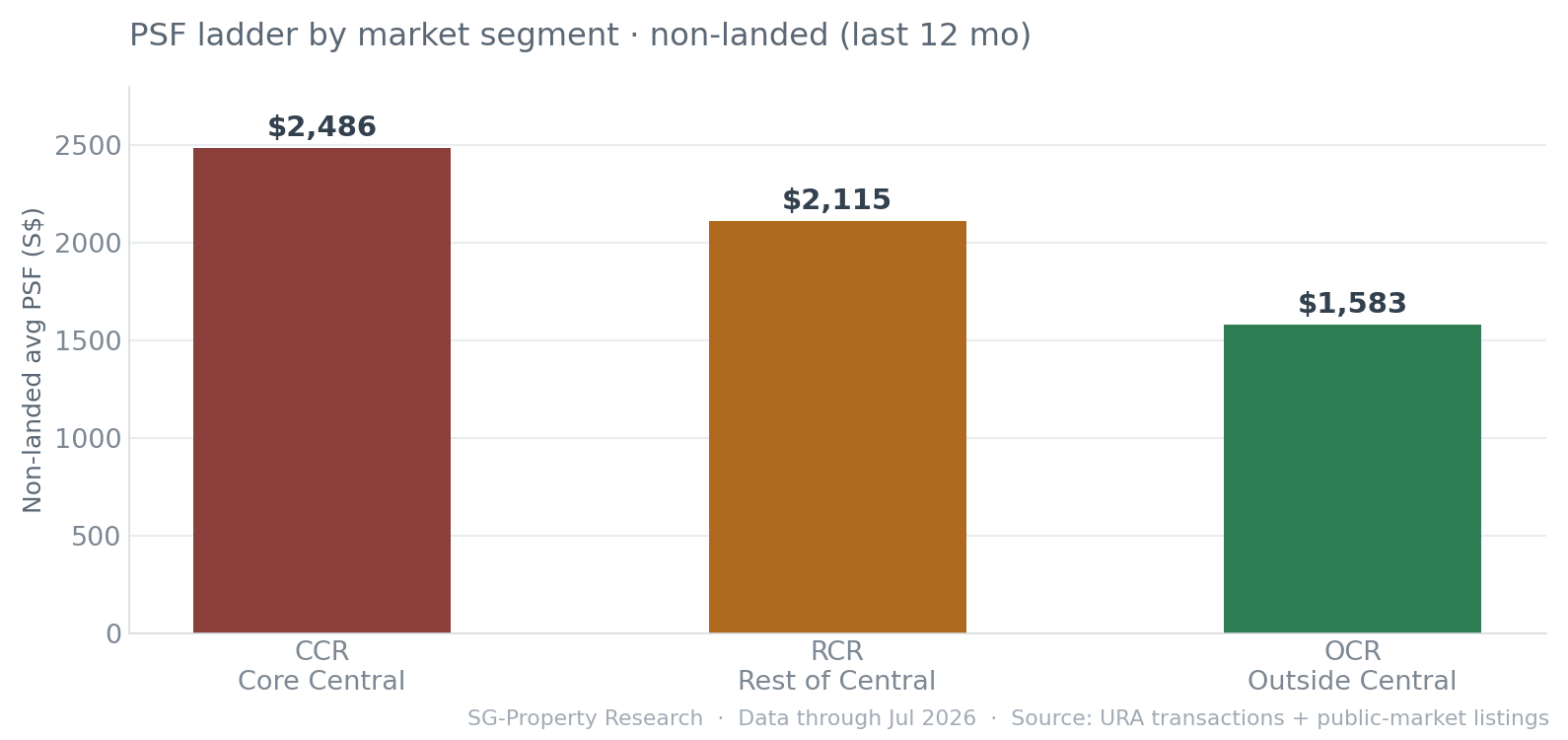

- Segment divergence: OCR resale absorption of about 23 months is the most active, while CCR at about 72 months is the hardest to clear; the average PSF ladder runs CCR $2,486 › RCR $2,115 › OCR $1,583.

- Category mix: condos about 78%, ECs about 12%, landed about 8%; for each category's trends, see the deep-dive report links at the end.

Market Overview

Over the past five years, Singapore's private residential market has steadily expanded in volume and climbed in price, with non-landed homes (condos and ECs) as the overwhelming majority.

Annual transaction volume rose from about 19,000 units in 2021 to about 30,000 units in 2025; non-landed homes make up more than 90% of this, while landed homes total roughly two thousand a year — scarce and infrequently traded. On price, the non-landed average transacted PSF climbed steadily from $1,619 to $2,078, a five-year +28.4% (flattening only slightly in the first half of 2026).

New Sale vs Resale

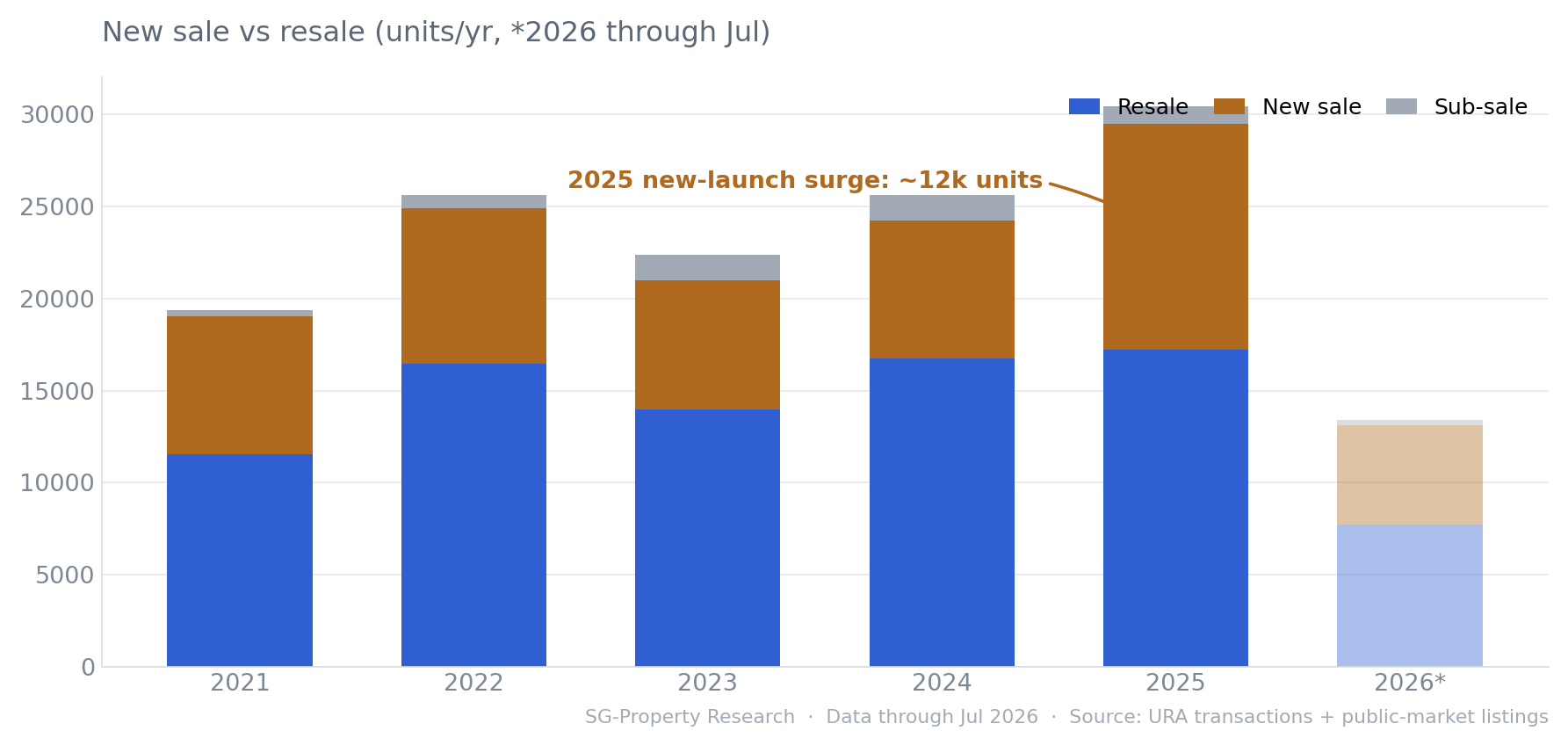

To understand Singapore's private residential market, you first have to look at "new sale" and "resale" separately — their rhythms and meanings are entirely different.

Resale is a continuous flow of secondary-market trades, whereas new launches are released by developers all at once, with transactions bunching together. New-launch transactions surged to about 12,000 units in 2025 (from about 7,500 in 2024) and, on top of the 17,000 resale units, together pushed the year's volume to a high. This wave — a "new-launch flood" — is precisely the key premise for understanding absorption.

The Absorption Truth

The commonly quoted "absorption period" lumps new launches and resale together — and this systematically overstates the market's true liquidity.

The reason: new launches are released in bulk and generate large short-term volume, inflating the absorption denominator and making the period look short; but those transactions do not reflect the absorptive capacity of resale supply. Using URA's type-of-sale field to strip out new launches and count resale only, the gap is startling: market-wide absorption stretches from 20 months on the "all-sales" basis to 38 months on the "resale-only" basis — nearly double.

By segment, OCR (Outside Central Region) resale absorption of about 23 months is the most active, with the strongest owner-occupier demand relay; RCR is about 49 months; CCR (Core Central Region) resale runs about 72 months and is the hardest to clear, where high quantums and a narrow buyer pool carry the greatest liquidity risk. The next time you see an upbeat "sold out in a few months" claim, it is worth asking first: is that new launch, or resale?

| Segment | Listing inventory | 12-mo transactions | of which resale | Absorption (all sales) | Absorption (resale only) | Avg PSF |

|---|---|---|---|---|---|---|

| CCR Core Central | 13,785 | 4,801 | 2,292 | 34 mo | 72 mo | $2,486 |

| RCR Rest of Central | 15,149 | 7,585 | 3,722 | 24 mo | 49 mo | $2,115 |

| OCR Outside Central | 14,371 | 14,057 | 7,645 | 12 mo | 23 mo | $1,583 |

| All market | 43,305 | 26,443 | 13,659 | 20 mo | 38 mo | — |

Strip out the "new-launch flood" and market-wide true resale absorption nearly doubles. When measuring liquidity, always separate new sale from resale — the same basis every deep-dive report on this platform uses.

Segments & Categories

Price is about segment, choice is about category — one chart to grasp Singapore's private residential price ladder and mix.

The non-landed average PSF forms a clear ladder: CCR $2,486 › RCR $2,115 › OCR $1,583, with the core region roughly 1.6× the suburbs. By category, condominiums/apartments account for about 78% of transactions, ECs about 12%, and landed about 8% — condos are the outright mainstay, ECs the subsidy-gated "sandwich" option, and landed the scarce apex.

Deep-Dive Reports

Beneath this overview, we provide a dedicated deep-dive report for each category — on a consistent basis and cross-referenceable:

Notes & Sources

- Transaction data

- URA private-residential caveats (volume, transacted PSF, type of sale, tenure, market segment).

- Listing inventory

- Live public-market (is_alive) listings, assigned to CCR / RCR / OCR by postal district.

- Absorption period

- Current listing inventory ÷ trailing-12-month monthly average transactions; "resale only" removes new launches (type of sale = new sale). Healthy benchmark ≤6 months.

- Non-landed / landed

- Non-landed = condominiums/apartments + ECs; landed = terrace/semi-detached/detached. PSF is based on non-landed.

- Market segment

- Uses URA's official marketSegment (CCR / RCR / OCR).

- Time range

- URA transactions on a rolling basis; this report uses 2021 to July 2026.

Cite this report

SG-Property Research Team, "Singapore Private Residential Market Overview: Transactions, Prices, the Absorption Truth & Market Segments (2021–2026)," July 2026.

https://sg-property.ai/reports/singapore-private-property-market-overview/en/

Want to know which segment and category give you the most for your budget?

Tell SG-Property AI your budget, preferred areas and preferences, and we'll combine live listings with URA transactions to surface low-premium, high-value homes for you.

Start asking AI for free →